Arithmancy Class

Forecasting at The Conversation

I took part in The Conversations’ annual forecast-a-thon where a group of economists try and predict how the economy will unfold in 2023. Hopefully we do a better job than last year when 2022 wrong footed almost everyone!

So how were my forecasts produced? I thought I’d unpack my process in this post.

Phone a Friend

When faced with a tricky problem, the first step one should take is to ask someone smarter than you. Fortunately I know 80 people smarter than me who regularly put out economic forecasts for the year, which should form the basis for any sensible forecast of the Australian economy.

These forecasts reflect the collective knowledge of the RBA, including detailed knowledge of the quirks of the data (for example advertised rents today can be used to forecast rents in the CPI tomorrow) and a large bank of models which are beyond the ken of any one economist.

But that should really only be the starting point for your forecasts for four reasons

Forecasts age like cheese and we have had almost 3 months of new data since the November SMP.

The RBA’s forecasting assumption might be wrong and/or out of date.

You might disagree with the house/conventional opinion that the RBA forecasts are based on.

This is more fun!

Revise and resubmit

There are two major data points that have dropped since the last SMP. First trimmed-mean inflation came in slightly hotter than expected (6.9 vs 6.5) given the strong persistence in inflation I have increased my profile for inflation over 2023.

Similarly recent immigration data suggests that population growth will be higher than was forecast at the last budget (which the SMP broadly follows). This shouldn’t impact inflation or unemployment, but it will mean a faster growth rate for GDP (and its components). I also upped the profile for wage growth as I just don’t believe that a big real wage fall is sustainable.

I put the probability of a recession in Australia at 10%. If growth is 1.6% over 2022 I think two quarters negative of GDP are unlikely, but it cannot be ruled out. I am slightly more optimistic on this front compared with other economists. Partly this is because GDP is somewhat negatively correlated on a quarterly basis. Weak quarters usually involve catch up growth in quater, which is why two negative quarters in a row is less likely then the weak annual figure might suggest.

Other variables aren’t forecast by the RBA however. Some of these predictions are provided by financial markets. The ASX publishes market expectations for the cash rate - while it takes a brave economist to try and outperform the markets I suspect the cash rate will be slightly higher than the median forecast. And of course the FX markets give their best guess of where the Australian dollar will be tomorrow (whatever level it is trading at today!).

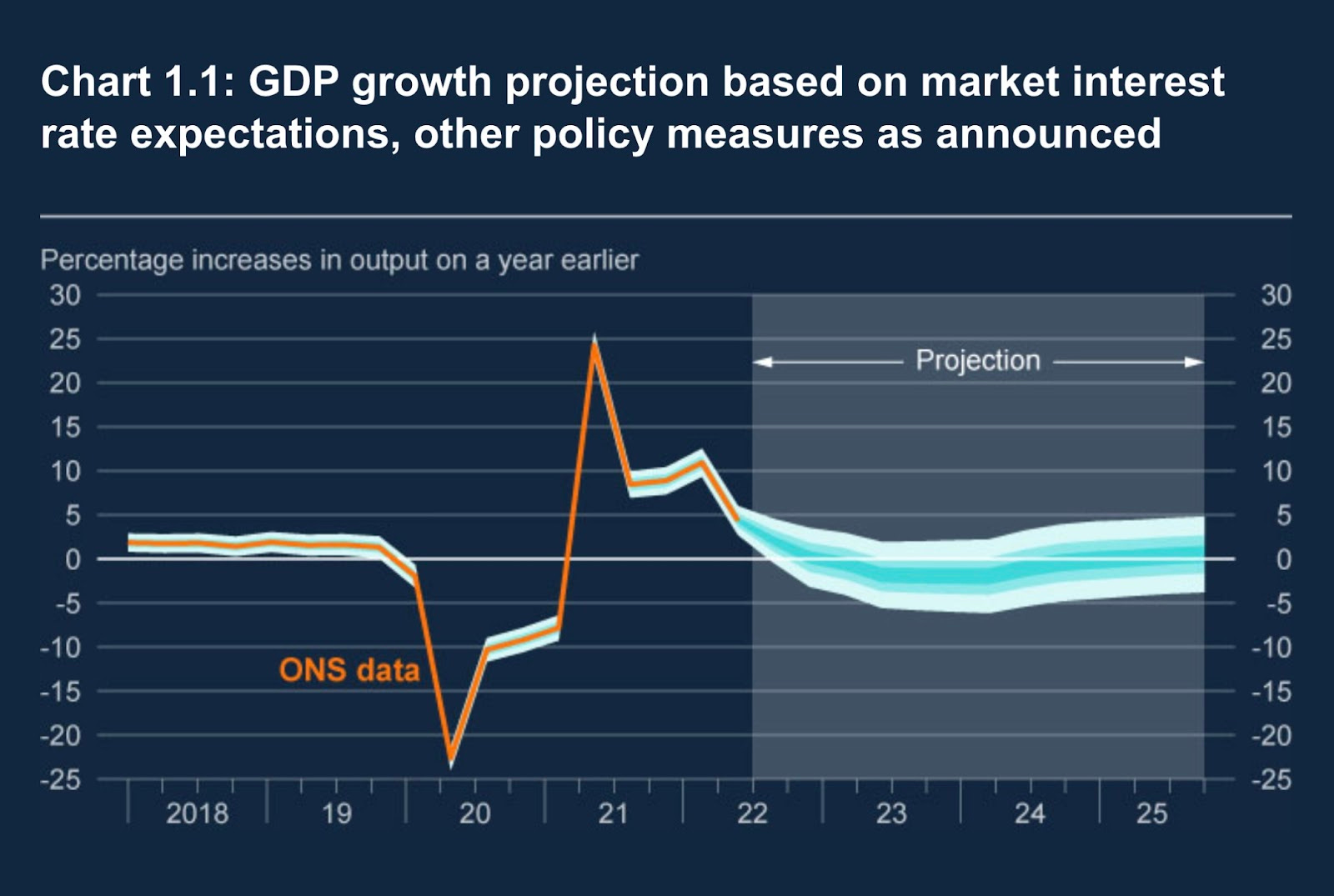

For foreign variables I turned to the respective central banks overseas, using their forecasts of GDP growth to gut-estimate the probability that two of them will be negative in a row. I was surprised by just how pessimistic the outlook is for other counties. The UK is forecast to have more than a year of negative growth, which is worse than the Eurozone. Even the Federal Reserve is pessimistic about the outlook in the US with GDP expected to grow by only 0.5% with significant downside risk!

Economists around the world have a gloomy outlook for 2023. Here’s hoping we are wrong.