Break out the platform shoes and vinyl because the 70s are back baby! Despite inflation being an anemic 1.1% in the March quarter, inflation concerns are breaking out everywhere.

Unsurprisingly much of these concerns seem to be imported wholesale from the US - which has recorded one month of genuinely high price rises - rather than any serious analysis of the Australian economy. So what is the outlook for inflation in Australia? Let’s break the issue into three related, but distinct, questions:

Is inflation going to rise from it’s currently low rate?

How does this compare to what was expected by the RBA?

Finally, what does this imply for monetary policy?

The only way out is up

Given the rock bottom inflation rate the Australian economy started with in 2020 it would be hard for inflation to do anything but increase over the rest of the year. The question is by how much. Unfortunately Australia remains one of the only two developed countries to measure inflation at a quarterly frequency. So the next official read on inflation won’t occur for two months!

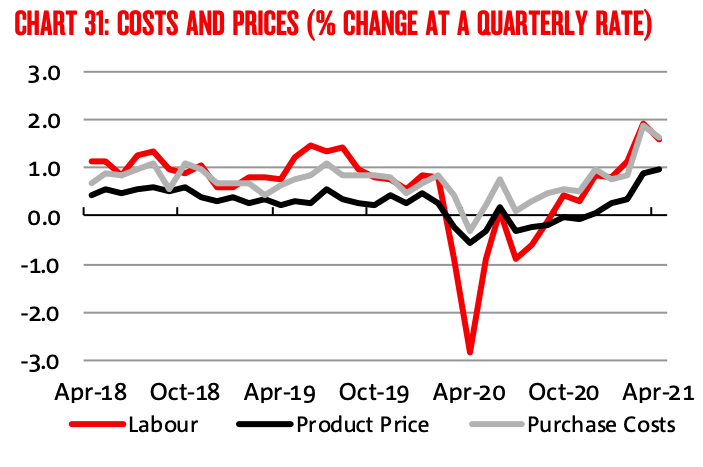

The next best indicator of inflation (indeed probably the best non-ABS monthly data release) is the NAB business survey. The monthly survey contains several estimates of price level growth and is relatively informative when now-casting inflation (at least it was when I was on the Business Survey desk at the RBA many years ago!)

The data from April suggest that inflation is indeed picking up in Australia, with the rate of price growth well above levels seen during 2020. Indeed the current print is higher than anything seen in the 2 years prior to the Covid crisis!

The same story generally holds for noisier retail price figures.

This suggests that price pressures are building and that we should not be surprised if inflation picks itself up off the floor in Q2.

It’s all part of the plan?

But how will this increase compare with the RBA’s expectations? The May SMP (published before the NAB survey was released) outlines the RBA’s thinking as of late April when the forecasts were finalised. In the May SMP the forecast for June 2021 year-ended core inflation was ~1.5% which implies a quarterly print of ~0.4%. This is a relatively low forecast implying plenty of slack within the economy and would be similar to the sluggish price growth Australia saw from 2016-19.

The NAB survey is only one data point, but the fact that product prices are now growing at their fastest rate in 3 years indicates that Q2 inflation may well end up higher than the RBA’s conservative forecast.

The Governor’s not for turning

What would an inflation rise mean for monetary policy? In all likelihood not much. The RBA has been below it’s inflation target for years and a faster return to 2-3 per cent would be welcomed by the bank. On the margin it may mean that Yield Curve Control is less likely to be extended in July, but unless core inflation prints at an extremely high level (say 0.8 or above) there won’t be a big change in policy direction and I would expect QE to continue to be rolled out in $100 billion dollar batches.

Covid-19 has transformed both the Australian economy and how policymakers manage it. Both Canberra and Sydney are committed to a march to 4.5% unemployment and they won’t be deterred by a little bit of long overdue inflation.