Interesting Reserves

Why the RBA is paying banks $14 billion a year

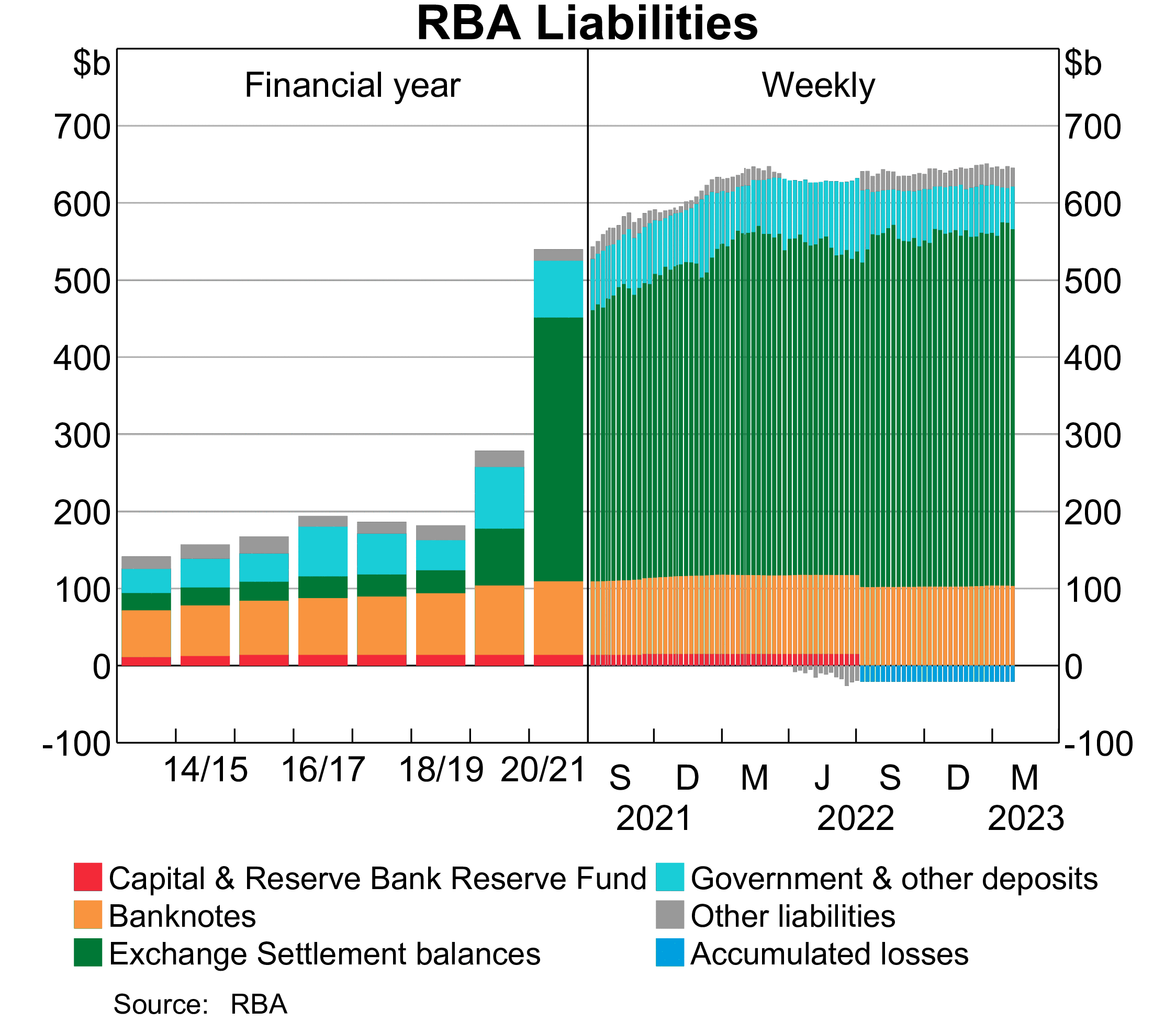

Since the onset of the pandemic the RBA has started paying a substantial amount of interest on exchange settlement balances. Exchange settlement accounts are essentially the banks’ bank accounts with the RBA. They can hold money there, transfer it between to one another or exchange it for physical coins and notes.

Since the RBA flooded the banks with cheap money to support the economy during the crisis changing the interest on exchange settlement balances has become the principal way the RBA affects interest rates in the economy. If they want to raise rates, they increase the interest rate they offer banks on their exchange settlements and the banks duly pass on the rise in rates to Australian borrowers (always) and savers (sometimes).

These ES balances fall into two types.

∼5% are required reserves (formerly known as ‘applicable minimum exchange settlement balance’) which banks are forced to hold and pay no interest.

∼95% are surplus balances (aka excess reserves), which were created largely due to the QE program and pay an interest rate that is 0.10% less than the current target for the cash rate.

Today the RBA pays the 3.25 per cent on all excess ES balances (which are around $443 billion)! This adds up to over $14.4 billion per year of public funds- a substantial sum! Furthermore this interest bill will increase by around $1 billion for every 0.25 per cent increase in the cash rate.

Sometimes in the world of finance and banking it is hard to know when a number is unreasonably large or just the inevitable result of a large industry that serves 26 million Australians.

Eyeballing the RBA’s chart pack, the banking sector made roughly $35 billion profit last year after tax. This means that the RBA’s interest payments on excess settlement balances are currently running at around 40 per cent what the banking sector made in profits last year. And this number is only set to rise as the RBA tries to rein in inflation with higher interest rates.

The good news is these payments are avoidable. The UK is struggling with a similar problem and recently the IFS has discussed deploying a system of tiered reserves to reduce the burden on the taxpayer.

The basic idea is pretty simple. The RBA would raise the level of required reserves (which pay no interest), mechanically reducing the surplus balance in exchange settlement accounts which receive a 3.25 per cent interest payment. This would instantly reduce the interest payments the RBA is currently sending to the banking sector saving the taxpayer potentially tens of billions of dollars.

A small amount of reserves would still receive a positive interest payment which would allow them to set interest rates as per usual.

The IFS report outlines a lot of the technical details behind such a move including exactly how one would set the required reserves for each bank, how monetary policy would be implemented and how a future bout of QE would be implemented (or unwound).

No free lunch

This is of course not a free lunch.

Stripping banks of their interest payments would decrease their profits (and the dividends of those who own the banks) similar to the Major Bank levy the Coalition introduced in 2017.

Indeed reducing interest on reserves might work a bit like a bank tax. However, depending on its design, it could be lump sum in nature and thus would be a relatively efficient tax - something economists generally support. It could also be tailored to distinguish between the four big banks and their smaller competitors to encourage competition in the market for money. More generally while the RBA could halt all of the $14 billion dollar payments, it would likely not be optimal for financial stability reasons.

A second concern would be how it would affect future episodes of QE. The RBA would need to announce a plan for how it would implement any future asset purchases. The most straightforward solution would be to announce that all future QE episodes would be conducted with non-interest bearing reserves only. This would be consistent with stopping paying interest on reserves today as well as minimising the risk that future QE episodes would generate large and unpredictable taxpayer losses in the future.

In an environment with high inflation, a cash strapped Treasury and a banking sector reporting “fat profits”, reducing interest on excess reserves could be a win-win policy. Helping to rein in inflation while also repairing the public balance sheet.

Dude, banks pay interest on customer liabilities which nets against the interest paid on reserves. The fact that the RBA bought several hundred billion dollars of fixed rate assets and funded them with overnight deposits from the banking system (ES) is not the banks fault, it’s Phil Lowes!

Interesting question as to why the ESA balances rate was not set at zero in March 2020. While a corridor system necessarily collapses to a floor system at the zero bound, the subsequent reduction in the target rate to 0.1% and ESA rate to zero shows that the claimed ELB at 0.25% was a self-imposed policy constraint rather than a technical or operational one.