Last week’s post was a bit unfortunate as new data on median earnings for 2024 was released only one week later. So I thought I would check back in and see if this more recent data had changed the outlook for how the average worker is tracking in today’s economy.

Fortunately it seems that in 2024 median wages still grew strongly. Median earnings across all employees grew by a whopping 7.4 per cent and limiting the sample to full time employees average earnings grew by 6.3 percent - both well in excess of inflation over the past year or so.

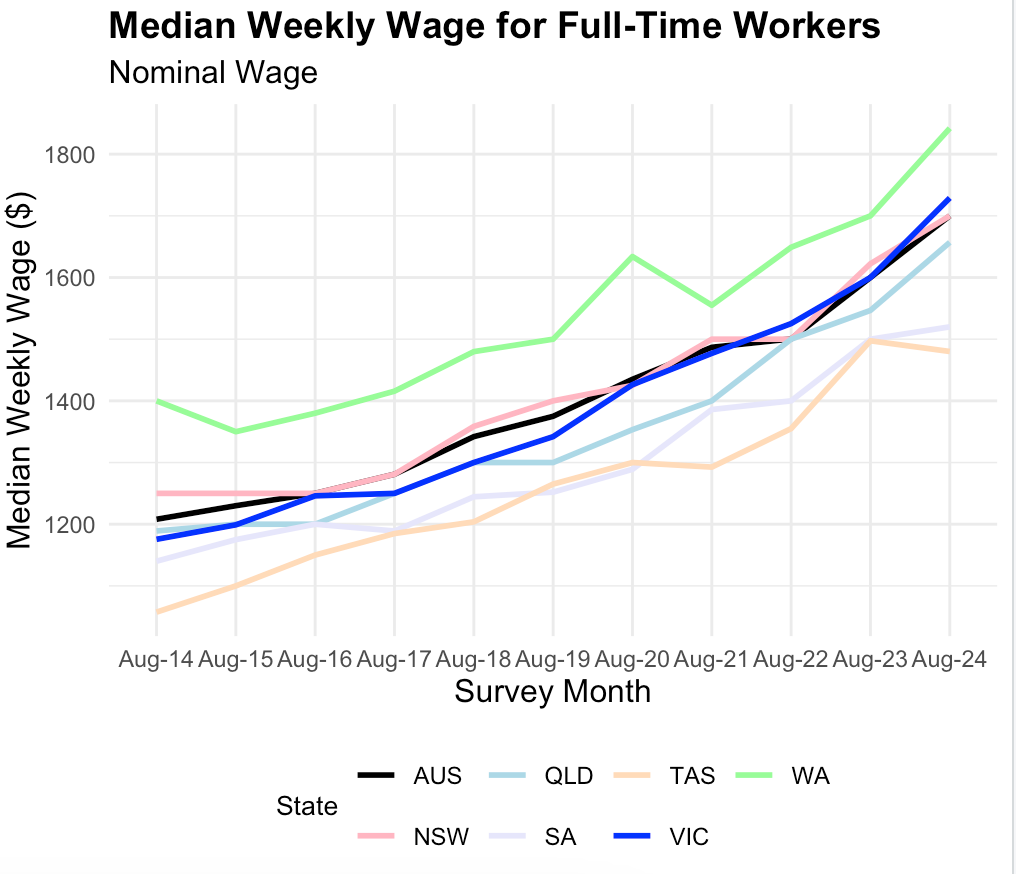

Breaking down the results by state we can see that the supposed basket case Victoria still seems to be performing strongly, with the median weekly full time wage now above the nation as a whole and even out performing NSW!

I have to be honest these figures surprised me as they run counter to the narrative - especially in my home state of Victoria. Now you might think that this is data mostly about the past and that the fiscal outlook will mean that businesses and jobs will be fleeing the state in the near future. But outside of press releases by the Business Council I don’t think there is much evidence for that either.

Compared to 2019 self reported expectations about non-mining business investment has soared by 44 per cent, second only to WA and basically the same as NSW. This is particularly impressive as Victoria slipped in terms of its population share during the pandemic. This reflects what businesses actually plan to spend in the future - concerns about the current debt and deficits do not seem to be holding back Victoria.

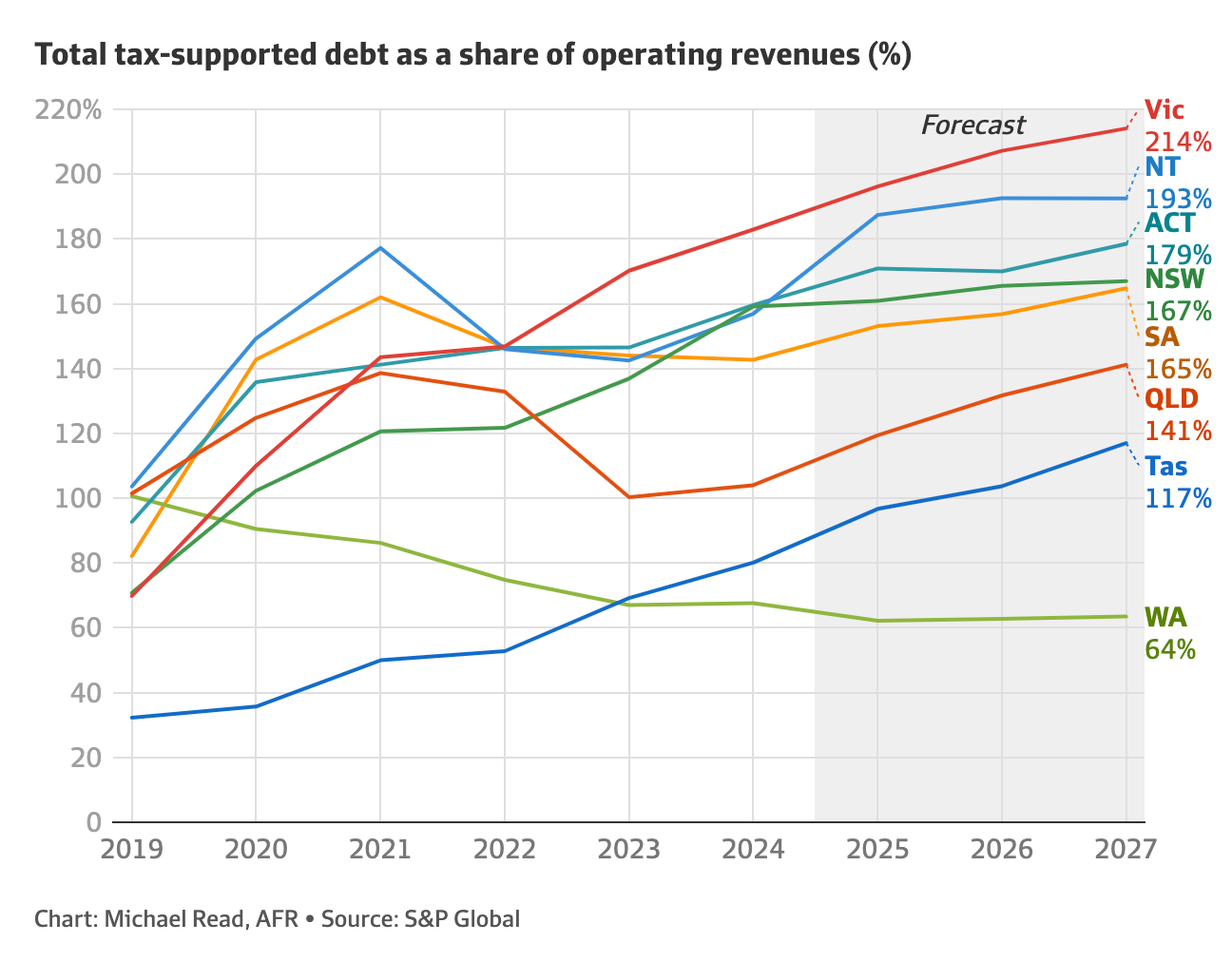

At least not yet. It certainly remains the case that Victoria’s debt remains the highest of all the states and growing fast. So why does it not seem to have led to worse economic outcomes?

I have a couple theories. The first is that a lot of this debt was racked up during the pandemic, and while this part of the debt burden will require costly taxes to pay it back it doesn’t represent an active and on-going misallocation of resources today.

Second is that the taxes that have been increased to help pay off this debt (namely land tax and payroll tax uplifts) are generally considered the more efficient sort of taxes at the government's disposal and will have a relatively smaller burden on the economy as a whole.

Third, these areas that are being taxed are being affected (we are starting to see some slippage in building approvals for example which may reflect weaker investor demand), but that the effects are largely quarantined to this segment of the economy.

This is not to say that fiscal rectitude is not important. There is an upper limit to how much you can tax without eventually affecting the economy even with relatively efficient taxes. And once you reach that point the only other fiscal alternative is spending cuts, which even if they don’t decrease GDP can certainly affect living standards. But talk of an economic blackhole south of the Murray is premature to say the least!

Thanks, very interesting data and analysis.

I'd be more interested in the median weekly wage for all workers.