Navigating the NAIRU

Crazy idea: how about we ask a model?

A recent survey in The Conversation highlighted the current level of disagreement regarding one of the most important macroeconomic estimates: the Non-Accelerating Inflation Rate of Unemployment aka the NAIRU.

With unemployment at record lows and inflation finally starting to descend several survey respondents have speculated that the NAIRU has fallen to historically low levels perhaps even starting with a 3! Which would be great news! If we can sustainably achieve lower levels of unemployment without risking higher inflation social welfare will be unambiguously higher.

But is it true?

Model answer

While gut estimates certainly have their place in economics, there is no substitute for using a formal model to approximate the economy - even if it is not the final word.

Using David Stephen's code that estimates the NAIRU (using Matt Cowgill’s great readabs and readrba packages), I replicate the RBA's 2017 Bulletin article on the NAIRU by Tom Cusbert.

Complete replication isn't entirely possible, as the Bulletin article uses a variety of inflation expectations that, as far as I can tell, aren't publicly available. However, by estimating the model over a shorter sample starting in 1986 and filling in a few gaps, a decent approximation of the original model can be created. Instead of using maximum likelihood as the RBA does, I took a Bayesian approach and used their estimates to inform my model's priors. This way, even though my model doesn't extend all the way back to 1968 as theirs does, I can use the information from their estimates to inform my own model.

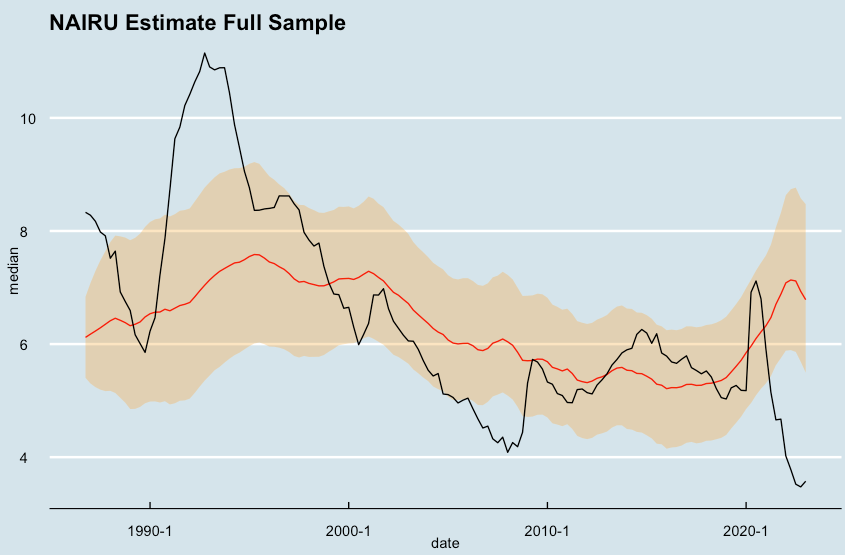

As an initial check I first estimated the NAIRU over the pre-COVID period. This result aligns fairly well with the results from the Bulletin article. The NAIRU started off at around 6% in 1986, rose during the early 90s recession, and then slowly declined from 1996 onwards. While there are some differences, considering the wide error bands attached to both models their results align fairly well.

Notably, we find that going into the COVID-19 pandemic, the NAIRU was around 5%. Extending the sample to include the past three years significantly changes the estimated NAIRU primarily due to COVID-related inflation.

Although the original model includes some measure of overseas supply shocks, they are poorly suited for capturing the pandemic's effects. Being unable to incorporate the supply shocks the model tries to explain the recent high inflation levels as being caused by a very large negative unemployment gap, which necessitates both a fall in the unemployment rate as well as a rise in the NAIRU. This is what is required if you assume that the entirety of the recent inflation is demand driven! Of course this is not particularly realistic - we know there have been some very large supply chain effects!

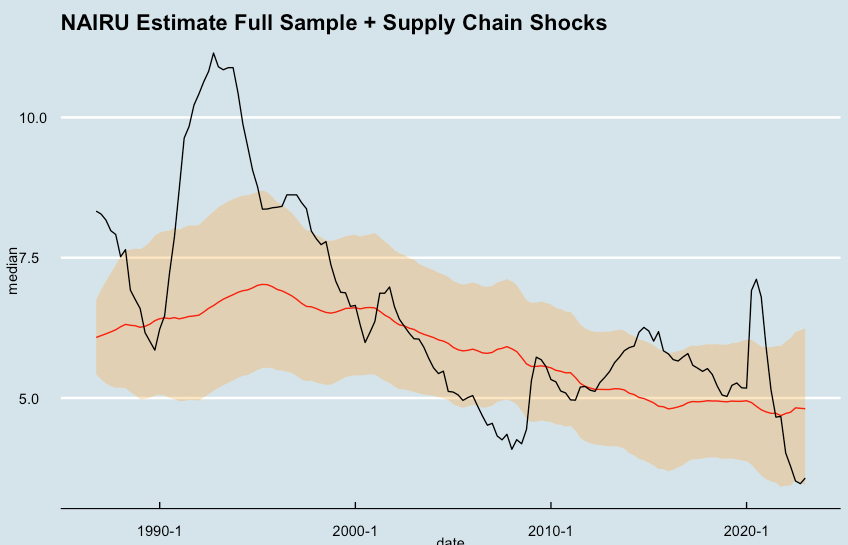

To resolve this problem I augmented the model to incorporate the Federal Reserve's measure of supply chain disruptions (shown below). After a bit of experimentation I include the index in both linear and quadratic terms with two lags.

This addition surprisingly works quite well!! With these non-linear supply shocks incorporated, the estimated NAIRU remains largely stable over the pandemic period. Despite all the volatility the combination of the supply chain index and the unemployment rate seemingly describes both the initial fall in inflation and its recent surge.

After declining for two decades the model estimates that the NAIRU has been steady in the mid-to-high 4%s for the past five or six years, with the latest point estimate being 4.8%. The 95% probability range is wide, stretching from 3.4% to 6.2%.

However, I believe it is sensible to focus on the midpoint of these estimates. This suggests that the NAIRU most likely remains in the 4s and hasn’t fallen as low as 3.5%, contrary to some economists’ confident predictions.

Of course, this result may change as more data becomes available. The full sample only extends to the first quarter of 2023, and we will have many more quarters before inflation fully returns to target. That being said, this is, in my view, as close as we can get to estimating the current NAIRU in real time.

When the facts change, we should all change our minds. But as of now, there seems to be little evidence that the NAIRU has changed significantly despite the economic fluctuations witnessed over recent years.

Hey Zach - great analysis. Are you able to share your code in how you have done this? Did you make any changes to the Stan code at all?

Fantastic analysis