Revisiting the RBA's target

Does NGDP targeting live up to the hype?

What economic variables should the RBA target when setting monetary policy?

Traditionally the RBA has targeted a mix of inflation and economic activity (usually measured by the unemployment rate). More recently there has been a push to switch towards having the RBA targeting Nominal GDP in order to better stabilise the economy.

To help shed light on how different targets would impact monetary policy, I spun-up the RBA’s main model of the economy, MARTIN, to estimate how monetary policy would change under different cash rate targeting rules.

In the baseline version of the model the RBA sets the cash rate in response to the trimmed-mean inflation rate and the unemployment gap in roughly equal measure. I model three alternatives to this baseline.

An inflation targeting RBA which places zero weight on unemployment and only responds to changes in core inflation.

A nominal GDP-targeting RBA which sets the cash rate according to variations in NGDP. A higher (lower) rate of NGDP growth leads to the RBA increasing (decreasing) the cash rate.

A nominal domestic final demand (DFD) targeting RBA which sets the cash rate according to variations in nominal domestic final demand. A higher (lower) rate of NDFD growth leads to the RBA increasing (decreasing) the cash rate.

What is the nominal domestic final demand I hear you cry? It is essentially a measure of nominal gross domestic product that excludes both imports and exports (and inventories) - it thus is a measure of total domestic output, summing up consumption and investment from both the public and private sectors. It excludes the more volatile net exports term.

To compare how the different targeting rules perform I calculate impulse response functions for four shocks. This will show how the economy responds when an exogenous shock hits us requiring the RBA to step in to help stabilise the economy.

An exogenous increase in world commodity prices (ie iron ore). This is perhaps the canonical shock for the Australian economy due to our large, commodity export sector.

An exogenous increase in world agriculture prices that Australia also exports (ie wheat).

An exogenous increase in housing costs. This shock pushes up rental prices and thus house prices.

An exogenous increase in inflation expectations, which is the best analogy I could find for a traditional “mark-up” shock that increases inflation while decreasing output in MARTIN.

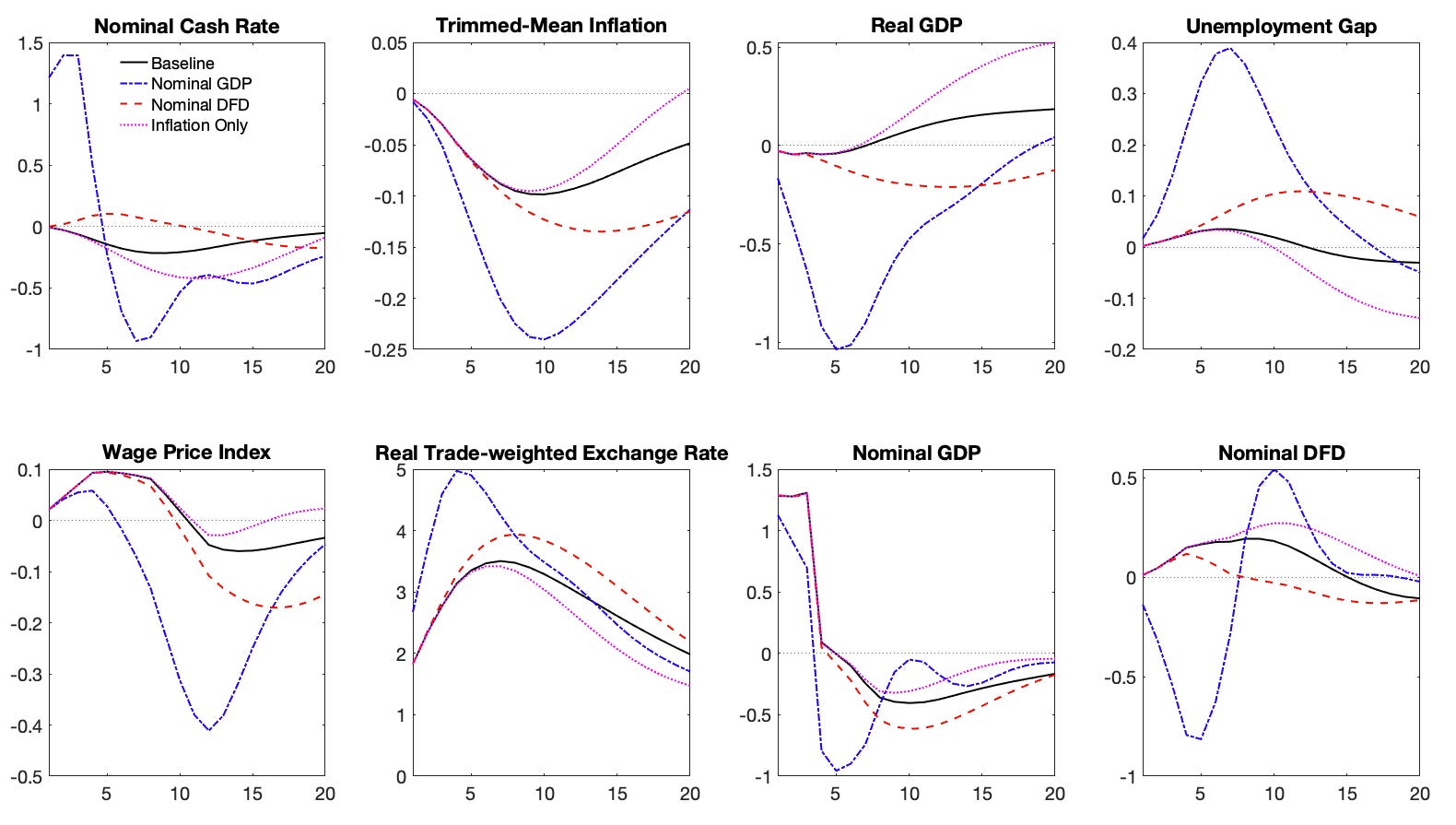

Shows us the charts!

What happens when we increase the world price for iron ore?

At first you might be confused by results from this commodity price shock as across every calibration inflation falls and the unemployment rate rises. Needless to say this is not the conventional narrative of what happened during the mining boom!

What is MARTIN thinking?

This is because the mining boom was driven by a large and permanent increase in commodity prices that in turn drove a substantial increase in investment in the mining sector.

However a transitory commodity shock (caused perhaps by temporary flooding in a Brazilian mine) will generate quite different results. Because of the long lags involved in investment in new mines companies such as BHP and Rio will only invest if they expect prices to be permanently. If prices rise for temporary reasons they are more likely to sit back, enjoy the higher profit margins and leave their demand for capital and labour largely unchanged.

So while a temporary rise in commodity prices pushes up the total nominal value of Australia's commodity exports, most of that value is captured by the mining firms and their owners. Because the supply of iron ore is relatively inelastic in the short run the real (i.e. price adjusted) change in commodity production is close to zero.

However the boom in commodity prices does lead to higher demand for our dollar and thus an appreciation of the exchange rate. This appreciation creates a drag on the non-mining export sectors which are now rendered less competitive. It also lowers the price of imports and thus reduces demand for goods produced by domestic firms. The combination of ~0 change to the real output in the mining sector and the Dutch disease-like response in the non-mining sector driven by the appreciation of the Australian dollar leads to a reduction in real GDP and a fall in the total demand for labour!

Thus initially the increase in the world commodity price leads to the unemployment rate rising. The combination of a higher unemployment rate and cheaper imports leads to a reduction in the change in the inflation rate.

A combination of high unemployment and low inflation means in the baseline calibration leads the Reserve Bank of Australia to actually lower the nominal cash rate in response to a commodity price shock.

However this is not true of all counterfactuals. While the pure inflation targeting RBA also cuts their cash rate, a monetary policy rule focused on NGDP would aggressively hike the interest rate - despite the falling inflation and employment levels.

This demonstrates one of the most common key critiques of NGDP-targeting a small open economy commodity export. While a price increase does not change the amount of iron ore Australia exports, it will increase its total value. Thus while real mining exports are unaffected by the shock, nominal exports (and thus nominal GDP) will be much higher. So when the RBA targets NGDP it not only increases the volatility of the cash rate, it actually leads it to move in the opposite direction to what would be required for central bank mandated with stabilising inflation and output.

Can NDFD do better?

What about a central bank that instead ignores nominal exports and uses the cash rate to target nominal domestic final demand instead? This greatly reduces the size of the nominal cash rate response - see the red dashed line. However, nominal domestic final demand still increases in response to a commodity price shock driven by higher levels of household consumption.

Nominal DFD targeting thus calls for higher interest rates even while inflation falls and the unemployment rate increases, which isn’t still ideal even if it is an improvement on NGDP targeting.

This analysis obviously abstracts from a whole range of factors.

Different expectations forming under different targets - MARTIN abstracts from any forward looking expectations

The costs of any regime transitions.

The possibility the MARTIN is mis-specified

The difficulties of revisions in the National Accounts data

Communication challenges (especially with less known concepts such as NDFD).

But as a back of an envelope calculation of how NGDP-targeting would fare in Australia (or even its less volatile sibling DFD) I think it shows that there are serious concerns with the proposed regime.

This post is already long enough! So I will unpack the next 3 shocks in a future post.

Thanks Zac!