Back to the Future

Back to the Future

Forward guidance should probabilistically be brought back

Forward guidance was an important tool in the RBA’s policy suite during the crisis, allowing them to signal that interest rates would remain low in order until the economy recovered. But even though Australia’s dalliance with the zero lower bound has ended that doesn’t mean the RBA’s embrace of forward guidance needs to.

Indeed other central banks like the Federal Reserve still engage in a similar exercise with projections for interest rates published in the statement on economic projections. The RBA already practises this informally issuing vague statements on the likely future change in the cash rate - witness the ongoing debate about whether the phrase “further increases in interest rates will be needed over the months ahead” means 2, 3 or more cash rate hikes and over what length of time. Vague phrases do little to communicate the RBA’s intentions and increase the amount of uncertainty over policy.

But the RBA could embrace a more rigorous approach by publishing probabilistic projections for where they expect the cash rate to be over the forecast horizon. Formalising these projections would be beneficial for a number of reasons.

It gives households a sense of how the cash rate will unfurl, giving them the ability to plan for future changes to their household budget.

It allows them to more clearly communicate their intentions about the cash rate. Instead of having people parse what is meant by “further increases in the cash rate will likely be required”. Monetary policy should not turn on the use of plural or singular adjectives in the statement!

It would provide more transparency about the cash rate path their forecasts are conditioned on.

It would communicate the inherent uncertainty around their projections and the potential changes.

It builds credibility for when forward guidance is most needed - when interest rates are constrained by the zero lower bound.

It would encourage the Board to think about the cash rate in a consistent and systematic manner.

It would lessen the degree to which press speculation will create new narratives about expectations for future rates based on a poor understanding of the RBA’s thinking.

Trust issues

A cynical central banker might wonder why anyone would take them seriously in the aftermath of the “3 years of low rates” guidance. And I have no doubt that many commentators will make exactly this point when such projections are first announced.

But I wouldn’t let that worry them. First, some people will rightly recognise the post pandemic period as being unusually volatile and expect the RBA’s future projections to perform much better than recent experience might suggest. I suspect those that matter most (journalists, market economists and other policymakers) will largely fall into this camp.

But it is true that others will discount the RBA’s statements about the future path for the cash after previously being burnt. That’s fine. Starting the process of forward guidance with low expectations means that it will be harder for the RBA to disappoint these people for a second time! And in time a track record of better projections will in turn build greater confidence in the process. If anything this highlights the importance of starting such an exercise today. If you think that forward guidance is distrusted by the Australian public you should be more inclined to start building up a better track record in advance of the next time the zero lower bound constrains the cash rate.

Home brew projections

What would these projections look like?

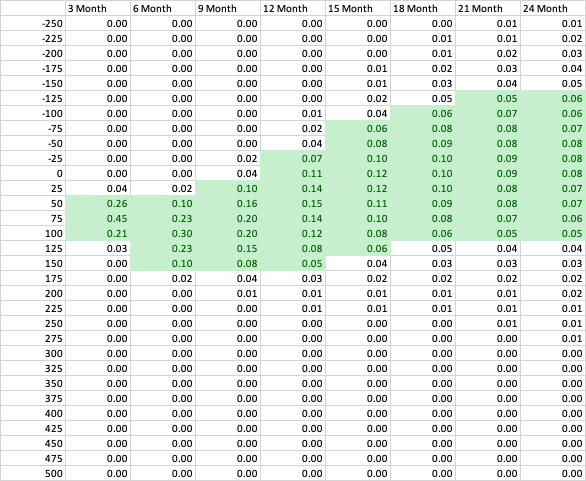

You can calculate a fairly reasonable baseline set of probabilistic projections using financial market expectations and their historical errors. I did a similar exercise last year (note how accurate the cash rate futures were, predicting today's cash rate almost bang on 9 months ago!). Limiting the projection to 0.25% buckets and assuming that errors are normally distributed gives you the following raw data

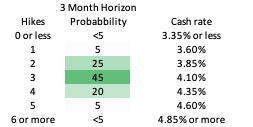

Focusing on the next 3 months you can see that the market confidently expects that there will be 2-4 cash rate hikes with 3 being the most likely outcome at 45% probability. In practice the RBA would likely adjust these regression-based estimates based on their judgement. For example 4 hikes over the next 3 months implies an unlikely return to 50bp hikes which the RBA might not wish to signal. This is similar to the RBA forecasting process in which models provide a baseline from tweaks can be made reflecting a range of other factors.

The great thing about a probabilistic projection is that it can never be definitely proven to be incorrect. Even if something truly unexpected happens which causes the RBA to cut the cash rate (or hike by 2%) those probabilities are still represented in the projection below (albeit at a less than 5% probability).

I can understand why the RBA will be reluctant to open themselves up to criticism by publishing hard numbers that may change over time or be criticised by those who dislike higher interest rates. But giving households a better sense of the range of possibilities is crucial to letting them plan for the months ahead while trying to tread the narrow path towards a soft landing.