Confusion with Counterfactuals

Structural changes matter much more than one off deviations

A smart friend of mine recently asked why we weren’t discussing counterfactuals for interest rates. If this was any other area of public policy we might model a couple possible policy choices (in this case different paths for interest rates), calculate the implications for key outcomes (ie inflation and unemployment) and then we could have a debate about which path is best.

A lower cash rate might mean higher inflation, but if it is only a little bit higher then maybe it is a trade-off worth making if it means fewer households are forced to sell their homes or lose their jobs.

I think such counterfactual analysis could in theory be quite useful, and the RBA should do more quantitative analysis rather than relying on qualitative descriptions of why higher interest rates are needed. But I want to outline one reason why such an exercise can be quite difficult in today’s volatile economy.

The DSGE is in the details

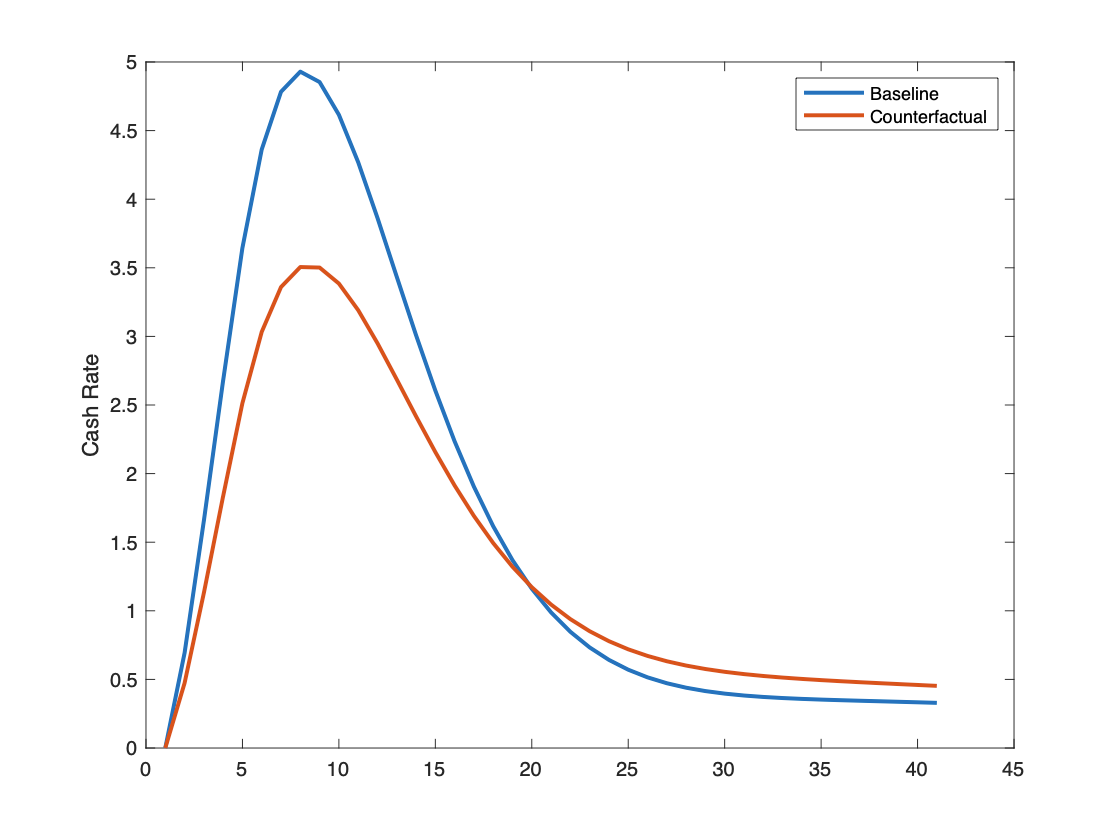

Consider a hypothetical inflationary boom as modelled by the RBA’s DSGE model in which inflation and output are driven up by an exogenous increase in government spending. The baseline calibration of the model calls for higher interest rates to offset the demand generated high inflation and output.

In this arbitrary scenario interest rates peak around 5 percentage points higher over the course of 2 years.

But what if you want to consider a more moderate path for the interest rate? Take for example the following path that only peaks at 3.5 percentage points higher instead of 5. What does this more dovish approach mean for inflation?

There are two ways you could model this counterfactual.

You could have the central bank make a repeated series of “one-off” deviations from its usual policy rule to keep interest rates lower than they otherwise would be. In this counterfactual the underlying policy rule hasn’t changed the RBA has just repeatedly ignored it’s recommendations.

You could change the RBA’s policy rule such that it is systematically less responsive to deviations from its inflation target. Because the new policy rule calls for a less aggressive response to high inflation, interest rates don’t rise as high.

To use an analogy from the legal profession, Option 1 would be akin to judges ignoring sentencing recommendations when setting the punishment for criminals and instead giving everyone that comes before the court a lighter sentence using their judicial discretion. Option 2 would be akin to changing the sentencing recommendations such that everyone knows that convicted criminals will face a lesser degree of punishment.

Which way you model the counterfactual path for interest rates matters quite a lot as the chart below makes clear.

Even if you use the exact same path for the cash rate you can have substantially different outcomes for counterfactual inflation - in fact the impact on inflation can be up to twice as large if you assume that the policy rule has structurally changed (the red line) as opposed to due to a series of one-off shocks (the dashed yellow line). This is because structural changes to the policy rule affect household and firm expectations’ about the future conduct of monetary policy.

Now generally when a central bank models alternative paths for the cash rate it (rightly) uses option 1 to estimate the counterfactual. Small changes to the interest rate, generated by one off changes to the policy rule. But the surge in inflation over the past year has been so large and swift that alternative paths for the cash rate might be better modelled using the second approach.

If a central bank kept interest rates at 3 per cent when a standard monetary policy rule calls for 5 percent is that really a one off deviation or a structural change in how monetary policy operates?

You get Turkey

Consider the most extreme scenario in which a (non-Japanese) central bank kept their interest rate at 0 per cent for the past year despite the soaring rate of inflation. One interpretation of such a policy would be that they have made a series of one-off policy changes to keep interest rates 3-4 percentage points lower than their policy rule would recommend. This interpretation would imply that inflation would be somewhat higher in 2023-5 (as the policy shocks affect the economy with long and variable lags), but would ultimately return to target in the long run. A second interpretation is that the central bank was no longer trying to target inflation at all in which case you get Turkey.

Ultimately nobody really knows for sure when a counterfactual path for interest rates moves from one-off deviations to structural changes in monetary policy. But clearly the implications between the two different interpretations can be extremely large, which is why estimating the difference between keeping interest rates at 2, 3 or 5 percent can be quite difficult.

You might enjoy reading this: https://warrenmosler.com/aframeworkfortheanalysisofpriceandinflation/

Especially sections 3, 5 & 6