The Cash Rate is Dead

Long live the cash rate

It was unheralded at the time (to be fair we had a lot going on) but one of the first casualties of the Covid-19 crisis was the market for Exchange Settlement balances at the RBA.

Exchange Settlement (ES) balances are essentially accounts that each commercial bank holds at the Reserve Bank. They are where monetary policy is actually implemented and how the RBA sets interest rates across the economy - or how they used too.

In the before-times each bank would use their ES account to transfer funds to one another. Over the course of each business day when their customers made transfers between the banks (say from NAB to ANZ) these transactions would be netted out and transferred via the ES balances at the RBA.

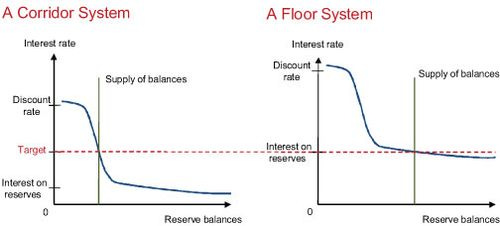

However the RBA kept the total size of ES balances relatively small and required each bank to hold a positive number in their account each night. To meet this requirement banks would regularly loan each other ES funds overnight so that each bank held a positive amount. These loans were at an interest rate called the “cash rate”.

The RBA set monetary policy by setting a target for this cash rate and adjusting the supply of ES funds to ensure that the target was hit.1

In March that all changed. In an effort to better support the economy the RBA flooded the banking system with ES funds, meaning that banks no longer had to scrounge to borrow funds to keep their balance in the black each day. There was plenty to go around even with the day-to-day fluctuations due to everyday banking.

Now few, if any, banks actually lend on the interbank overnight market. They have no need to. In fact almost half of the time there aren’t any transactions at all! The RBA instead has to use it’s expert judgement to determine what the cash rate!!

Today interest rates are determined by the RBA directly when it sets the interest rate it pays on these ES balances. So instead of refereeing the market between banks, it has simply announced the final score and sent the players home early.

This system (known as a “floor system” - as the interest on reserves acts as a floor below which interest rates cannot fall) is actually quite common around the world. It gained prominence in many countries during the GFC, but since then only one country - Canada - has “normalised” their monetary policy procedure and returned to an actively managed interbank market with limited reserves (this traditional approach is called a “corridor system”).

Will the RBA stick with their new fancy floor? Or will they revive the cash rate and return to the status quo? In theory both approaches should be equally efficient. While excess ES reserves have typically introduced in emergency situations when rates hit their effective lower bound, they are not synonymous and it is possible to operate a floor system with rates well above 0 per cent. The new approach is probably simpler to operate, and has worked well in the countries that have switched to it over the past decade, so they may well stick with the new world they have stumbled into.

In practice interventions were very rarely required as banks knew there was little point trying to offer, or accept, any interest rate other than the target cash rate.