The RBA is stuck in neutral

Getting mislead by the stars

Artwork courtesy of DALL-E.

TLDR: There are two different versions of neutral real interest rate (short-run and medium-run) which frequently describe the stance of monetary policy in opposite directions. The RBA seems to be confusing the two. This is bad!

In the latest minutes published by the RBA an entire section is devoted to a discussion of the neutral rate of interest. In it they describe what has lead the neutral rate to change over time (my emphasis added):

“Any development that affects the desired levels of saving or investment will affect the neutral rate. This includes slow-moving influences, such as trend productivity growth and demographic change, and more rapidly evolving influences, such as persistent changes in risk appetite.”

However I don’t think this is a correct description of the concept they are discussing.

There are a couple definitions of the “natural rate of interest” or more succinctly “r*”.

One definition outlined by Woodford defines r* as the interest rate (or path of interest rates) that generates price stability across all future periods. This is effectively the optimal path for policy which offsets other shocks to keep the economy close to its bliss position at all times (at least in a simple model of the economy). This is also known as the short-run r*.

Another definition of r* is outlined by Laubach and Williams (LW). They define r* as a medium term concept that ignores short term fluctuations in the economy. Their definition of r* is an attempt to estimate what the real interest rate is expected to be in a couple years time when it is equally likely the economy will be in a downturn or a boom. It is essentially an unconditional forecast of the real interest rate in the medium term aka the medium-run r*

Both definitions of r* are quite different. For example a transitory shock would impact Woodford’s r*, but not the LW’s r*. They also have different use cases.

The Woodfordian approach is very relevant for policymakers as it essentially lays out how they should set policy. However it is much harder to estimate and may vary considerably depending on which model is used.

The LW approach to r* is (in theory) easier to estimate since it only attempts to identity low frequency changes to r*. However it is also less useful as it only attempts to identify the expected real interest rate in the medium term - not what it should be today. It is best seen as a forecast of where interest rates will be in 2-3 years time or perhaps a guide for where interest rates should be if inflation is close to target and full employment has been achieved.

The RBA minutes seem to indicate that they are discussing the Woodfordian measure as it responds to “any development which affects desired savings and investment” which includes “rapidly evolving influences” such as cyclical fiscal shocks. This clearly indicates a more Woodfordian approach of incorporating all current shocks, as opposed to only long term structural ones per LW.

However all work published by the RBA on the topic (principally Rachael McCririck and Daniel Rees great Bulletin article on the subject) measures a LW-style medium term r*.1

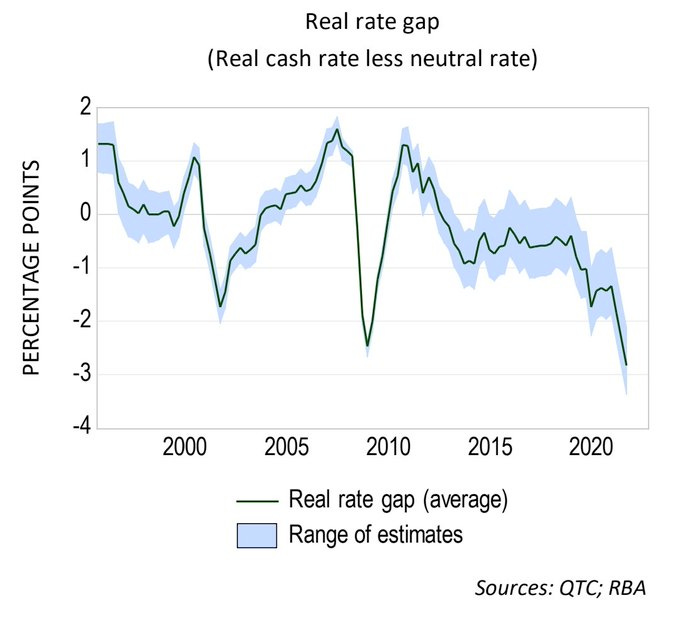

Why does this matter? Well consider the inflation undershooting that occurred in 2016-2019. According to the LW-style r* interest rates were substantially below the neutral rate as calculated by Trent Saunders and thus policy should be considered “expansionary”.

However during this period inflation was well below target and the unemployment rate was far too high. The Woodfordian interest rate, the rate required to keep inflation close to 2.5 per cent would have been substantially lower (as my work with Andrew Leigh shows). This indicates the monetary policy was actually too tight!

So the two different measures of r* would give you the opposite signal about the stance of monetary policy! One says “expansionary” the other says you are “too tight”! Looking at Trent’s graph it’s clear the medium term r* frequently gives confusing signals. For example in the pre-GFC mining boom monetary policy was measured as “contractionary” when inflation was running at 5% well above the target band! Indeed confusing the two measures may have contributed to a serious policy error as Stephen Kirchner discusses in a recent post.

Today’s economy with inflation well above the target band and unemployment well below any estimate of the NAIRU indicates that we should have a real rate well above the neutral interest rate. But judging by recent comments the RBA seems to be shooting to hit the neutral interest rate rather than aiming above it.

The Federal Reserve by contrast explicitly models both medium-term and shorter-run neutral rates and the two frequently diverge due to transitory shocks such as fiscal stimulus and changes in confidence that only affect the short-run estimates.

An expert in monetary policy should be able to keep these two somewhat contradictory concepts in their mind at the same time. But the Board is not filled with experts. Given the current composition of the Board I wouldn’t be surprised if the discussion of r* confuses more then it enlightens and consequently leads to poorer policy as a result.

Of course it is possible that the RBA has an alternative unpublished set of models which produced estimates for the Woodfordian r* that has been used solely for the Board but this seems unlikely.