Why are interest rates still so low?

ZIRP is not dead yet

The big question facing monetary policy makers around the world is how high to lift interest rates in response to the inflation surge. Should the RBA pause now at 3.1 per cent? Or somewhere close to 4 per cent?

One way to think about this problem is to take a Taylor or Monetary Policy rule and see what it suggests for the path of the cash rate. A Monetary Policy rule takes a couple key economic figures, such as inflation and the unemployment rate, and calculates the nominal interest rate that best balances the RBA’s twin goals of price stability and full employment.

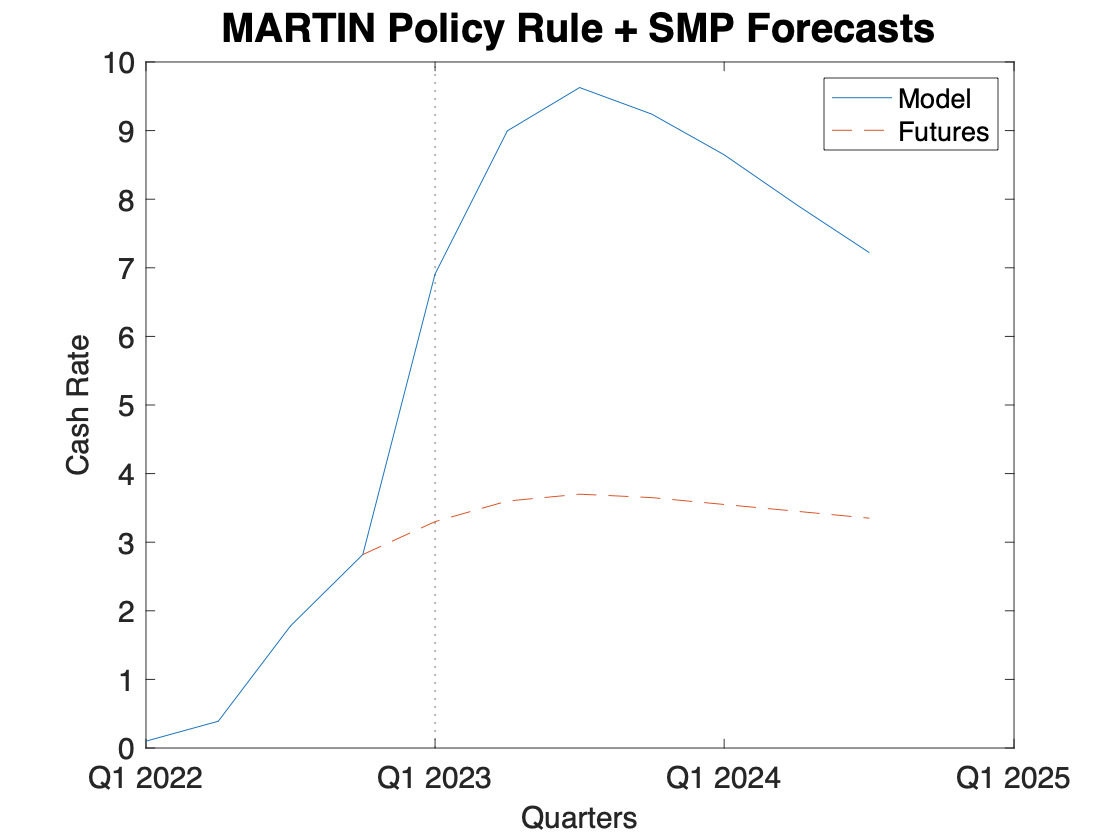

If you take the RBA’s forecasts1 for the unemployment rate and the trimmed mean inflation you can fill in the policy rule from the RBA’s model MARTIN (their most recently published version of such a rule) which lets you back out what the path for the cash rate should roughly be. Policy rules aren’t a perfect guide for interest rates, but they should be a decent approximation.

High interest account

Assuming a neutral real interest rate of 1 per cent, a NAIRU (essentially a measure of full employment) of 4.5 per cent and the rule’s standard calibration gives you a path for the cash rate that peaks at over 9 per cent!

Below is a graph of what the Taylor Rule suggests the cash rate should be, and what financial market futures currently expect.

Wild! Clearly this is an unrealistic path for the cash rate (I think??). This result is driven by the fact that inflation is really high and while the model focuses on trimmed-mean inflation to try and look past the quarter-to-quarter volatility a year of 4+ trimmed-mean inflation still calls for a dramatic increase in the cash rate.

Can we alter the policy rule to get a more reasonable outcome?

This turns out to be a rather difficult assignment.

Let’s start Lowering the NAIRU to 4 per cent. 4 per cent is towards the lower end of the range of possible estimates, but it is not crazy. Lowering it would thus produce a lower path for the cash rate. But the impact on the cash rate projection from lowering the NAIRU is fairly marginal.

The same is true of lowering the assumed value of the “neutral” real interest rate to only 0 per cent, from the baseline assumption of 1 per cent. But this still has a limited impact on the path for the cash rate.

Next I tried dialing down the weights in the policy rule, putting the coefficient on inflation to 1.5 (down from 2) and the weight on unemployment to 0.5 (from 2).

I even tried combining all three changes at once in a “kitchen sink” approach. This got close-ish, but still implied a cash rate over 5%.

Breaking the rules

One reason why none of these paths are not being followed is that there is a widespread view that the rise inflation is being driven by several temporary factors (one off oil price rises, one off real wage decreases etc) and that the true “underlying” inflation rate is lower than even the usually conservative trimmed-mean measure.

But I think the second likely culprit for the divergent projections is the assumption that the neutral real interest is 1 per cent.

This assumption that a 1 per cent real rate (which translates to a cash rate of 3.5 per cent in normal times) is roughly neutral is incongruous with a scenario in which a wild inflation boom and record strong labour market is resolved with a nominal interest rate peaking at around 3.5-4% as markets currently expect.

Depending on what inflation expectations you use this implies that the real interest rate will peak at 1-1.5% - if not lower.

If a real interest rate of around 1% is appropriate for once in a generation economic inflationary boom, I doubt it will be the on-going neutral real rate once we return to some form of normality.

Indeed when you look at the Federal Reserve's latest economic projections you see a much more consistent story. The Fed funds rate is expected to peak at 5% (~ 2.5% real) before decreasing to 2.5% in the long run (~0.5 % real). Increasing the real interest rate 2 percentage points above the neutral level makes sense if you are trying to reign in high inflation.

I suspect that the neutral rate is actually quite a bit lower than current estimates and that the long-run interest rate will return to something like the pre-pandemic secular stagnation with interest rates much closer to zero than their current levels.

We may have escaped the zero lower bound for now, but it seems more and more likely we will be back there in the years to come…

I used the soon to be redundant November forecasts. I doubt the picture will radically change though.

Plug the Survey of Professional Forecasters into the Taylor rule and you get Fed funds at 8.6% for Q4 22.